Last Updated: June 2026

If you have run payroll for any length of time, you have handed out perks that never crossed your mind as a tax issue. The holiday gift baskets. The pizza on a late night. The coffee in the break room. Good news: most of the time, you are right not to worry about them. The IRS calls these de minimis fringe benefits, and they are small enough that you do not have to track them, report them, or tax them.

But there is a catch, and it is the kind that catches people. Get the line wrong, and a perk you assumed was free and clear becomes taxable wages, which means a payroll correction you did not see coming.

This article covers what qualifies, the examples that can confuse people, how these benefits are taxed, and how they differ from fringe benefits that count toward prevailing wage.

Navigate This Article

- What Are De Minimis Fringe Benefits?

- Common Examples of De Minimis Fringe Benefits

- Are De Minimis Fringe Benefits Taxable?

- De Minimis vs Prevailing Wage Fringe Benefits

- Why De Minimis Fringe Benefits Matter

- De Minimis Fringe Benefit FAQs

What Are De Minimis Fringe Benefits?

A de minimis fringe benefit is any item or service you give an employee that has so little value that tracking it would be unreasonable or more trouble than it is worth. The term is Latin for "about the smallest things," which is a fair description of what belongs here: minor, occasional, and low in cost.

Two things have to be true for a perk to qualify:

- It has a low value.

- It is given infrequently.

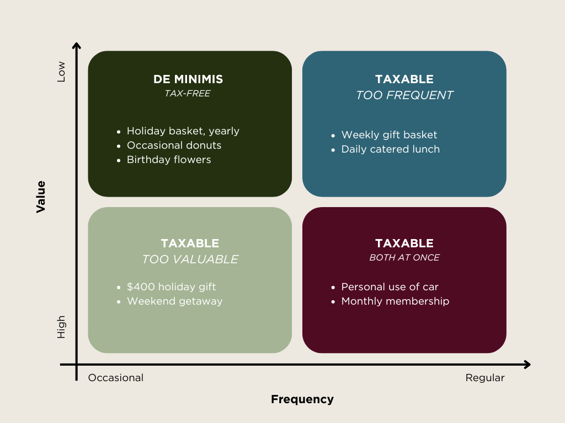

Here is where a lot of older advice gets it wrong. There is no fixed dollar limit for a de minimis benefit. You may have seen a "$100 rule" floating around, but the IRS does not set a specific dollar cutoff. Instead, it uses a facts-and-circumstances test that weighs both the value of the benefit and how often you provide it.

How Does the IRS Decide What's "Too Small to Track"?

The test is intentionally a judgment call. A $50 fruit basket given once a year is almost certainly de minimis. That same $50 handed out every week is not, because the frequency makes it look like regular compensation, and at that point, tracking is no longer impractical. Value and frequency are two sides of the same coin: the higher the value, or the more often a perk shows up, the less likely it is to qualify. One important catch to know: if a benefit crosses the line, the entire value becomes taxable, not just the portion above some imaginary threshold.

What Are Some Common Examples of De Minimis Fringe Benefits?

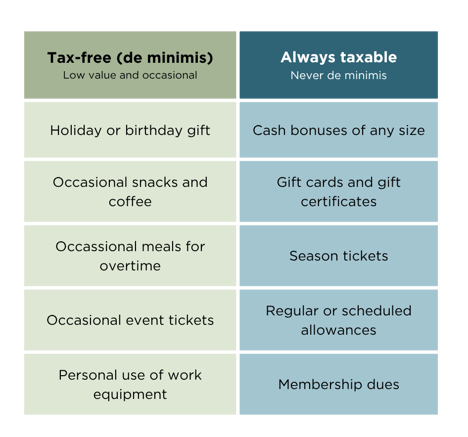

These generally qualify, as long as they stay low in value and are occasional:

- Holiday or birthday gifts with a low fair market value, like flowers or a fruit basket (not cash)

- Occasional snacks, coffee, and doughnuts in the break room

- Occasional meals or meal money when someone works overtime

- Occasional tickets to a game or the theater

- Personal use of an employer copier, or a work cell phone provided mainly for business reasons

- Small gifts like books or company logo items

A few that people file here by mistake: educational assistance is its own benefit category with its own rules and a far bigger exclusion, so it does not belong on this list. Occasional tickets are fine, but season tickets never are. And meal money or transportation only counts when it is occasional and tied to overtime, not a standing allowance you pay out every week.

If you want the full picture of which benefits are taxable and which are not beyond just the de minimis ones, our breakdown of taxable and tax-free fringe benefits covers the wider landscape.

What Does NOT Count as De Minimis?

This is where most employers slip up. Cash, and anything close to cash, is never de minimis, no matter how small the amount. That specifically includes:

- Cash bonuses of any size

- Gift cards and gift certificates (even a $10 card to a coffee shop)

- Charge cards or credit cards

- Regular allowances, or anything provided on a set, recurring schedule

- Season tickets and membership dues

If you hand an employee a $25 gift card as a thank-you, that is taxable wages. A $25 box of chocolates, on the other hand, is fine. It feels like a technicality, but the IRS is firm on it, so it is worth getting right.

Are De Minimis Fringe Benefits Taxable?

For your employees, no. A real de minimis fringe benefit is excluded entirely from their wages. It does not hit their W-2, and they pay no income or payroll tax on it. That is the whole reason the rule exists: everyone agrees these perks are too small to bother with.

For your business, you can usually deduct the cost of most de minimis perks as an ordinary business expense, the same as any other operating cost. One recent change to keep on your radar: the deduction for employer-provided meals through an on-site eating facility got phased out for amounts paid after 2025. So if you are feeding people at work, check the current treatment with your accountant before you bank on writing it off.

What is the Difference Between De Minimis vs. Prevailing Wage Fringe Benefits?

If you work on government or public works contracts, this distinction matters because the word "fringe" shows up in two very different places. De minimis fringe benefits are small, tax-free perks. The fringe benefits that count toward a Davis-Bacon or prevailing wage obligation are something else entirely: bona fide contributions like health insurance, retirement, or vacation pay that you document and credit against a required hourly fringe rate.

Here is the key takeaway: a holiday gift basket or a round of break-room coffee does not reduce what you owe on your prevailing wage fringe rate. The two do not mix. If you are trying to figure out what actually satisfies your fringe obligation on a public works job, that is a separate calculation, and our guide to calculating fringe benefits for prevailing wage walks through it step by step.

Why De Minimis Fringe Benefits Matter

For such a small corner of the tax code, these benefits pull real weight:

- They are tax-free on both sides. Your people keep the full value, and you skip the reporting.

- They keep your admin light. No tracking, no W-2 entries, no payroll tax math on a box of doughnuts.

- They are a cheap, genuine way to show you noticed. A small gesture at the right moment lands, and nobody gets a surprise tax bill for it.

The one thing to watch is frequency. The same perk on a regular, predictable schedule starts to look like pay, and the moment it does, it loses de minimis status and becomes taxable. Keep it occasional, keep it modest, and it stays simple.

Stay on the Right Side of the Rules

Since de minimis is a judgment call and not a bright line, you are going to hit gray areas. When a perk starts feeling too frequent or too pricey to really be "minimal," that is your signal to pause and check. A five-minute conversation with your accountant beats an unexpected payroll correction every time. And if you want it straight from the source, the IRS lays out its current guidance in Publication 15-B.

Staying on the right side of payroll and compliance rules is exactly what we do at Points North. If you are juggling fringe benefits, certified payroll, or prevailing wage reporting and want a few less things keeping you up at night, we are glad to help. Fill out the form below to request a demo of our software solutions.