Last Updated: June 2026

If you cannot file your ACA forms with the IRS on time, you can request a 30-day extension using Form 8809. It is a simple, one-page form, and for ACA reporting the first extension is granted automatically when you file it before your deadline.

Below, we walk through who can request an extension, what it does and does not cover, and what to do if the deadline has already passed.

Navigate This Article:

- What is an ACA filing extension?

- How do I request an ACA filing extension?

- When are ACA forms due?

- Frequently Asked Questions about ACA Filing Extensions

What Is an ACA Filing Extension?

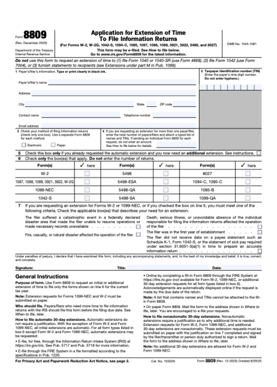

An ACA filing extension gives Applicable Large Employers (ALEs) an extra 30 days to file Forms 1094-C and 1095-C with the IRS. You request it by submitting Form 8809, the Application for Extension of Time to File Information Returns, on or before your original filing deadline.

One point to understand up front: this extension applies to filing your forms with the IRS only. It does not extend the separate deadline to furnish 1095-C forms to your employees. We cover that difference below.

How Do I Request an ACA Filing Extension?

To request your extension:

- Complete Form 8809. You can file it electronically through the IRS FIRE system or on paper.

- Submit it on or before your original IRS filing deadline. A late Form 8809 will not be accepted.

- That is it. For Forms 1094-C and 1095-C, the first 30-day extension is automatic. You do not need to sign the form or explain why you need more time, as long as you file it on time.

If you need a second 30-day extension, the process is different. A second extension is not automatic, requires a reason, and is rarely granted, so it is best to plan around the first 30 days.

When are ACA Forms Due?

Before requesting an extension, it helps to know the deadlines you are working against. ACA reporting has two layers: federal deadlines that apply to every ALE, and state deadlines that apply if you have employees in certain states.

Federal deadlines

For the current reporting year, the federal deadlines are:

- Furnish 1095-C forms to employees:

- If you are making the forms available to employees upon request, you must post a notice for employees, that includes how to request their 1095-C form, by January 31

- If you are planning to distribute 1095-C forms to all employees, either a paper or an electronic copy of the form, this must be completed by March 2. This includes the permanent 30-day extension from the original deadline of January 31.

- Paper file with the IRS: on or around February 28, available only to employers filing fewer than 10 total information returns.

- E-file with the IRS: March 31. Required for any employer filing 10 or more returns of any type combined.

Form 8809 extends the IRS filing deadlines above by 30 days. It does not extend the furnishing deadline.

State deadlines

Several states set their own ACA reporting deadlines, and some fall earlier than the federal dates:

- California: furnish to employees by January 31, then file with the state by March 31, with an automatic extension to file until May 31.

- New Jersey and Rhode Island: furnish by March 2, then file with the state by March 31.

- Massachusetts: furnish and file Form MA 1099-HC by late January.

- Washington, D.C.: file by April 30.

NOTE: State deadlines change periodically, and not every state offers an extension. For the full, current breakdown, see our ACA reporting deadlines guide.

Stay Ahead of ACA Deadlines with Points North

Filing extensions exist for a reason, and there is no shame in needing one. Still, the smoothest path is to keep your ACA data accurate throughout the year so deadlines arrive without the scramble.

That is what ACA Reporter from Points North is built to do. The software tracks employee eligibility across variable hours and multiple locations, generates accurate 1095-C forms, and e-files with the IRS using built-in validation to catch errors before they turn into penalties. Current IRS and state rules are updated automatically, so your team is not rechecking thresholds by hand every January.

Learn more about ACA Reporter, or contact Points North today with the form below to schedule a free demo and see how much simpler ACA reporting can be.